Long-term box rates have peaked: Xeneta

Xeneta has called out the peak for long-term contracted freight rates. The Scandinavian box freight rate platform has detected a slowing month-on-month growth for long-term rates in July, following many months of spot rates declining suggesting prices may have peaked. However, according to the latest Xeneta Shipping Index today’s valid long-term agreements stand 112% higher than this time last year, and a massive 280% up against July 2019.

Xeneta CEO Patrik Berglund said the signs were clear that there is a shift in sentiment.

July’s increases are the slowest since January, with upward pressure on long-term agreements easing as spot rates fall across major trades. In addition, volumes on many corridors are down, with, for example, containerised European imports down by 3%, and exports 6%, in the first five months of 2022.

“Indications are there that we may have reached a peak and that prices of new agreements are more likely to hold than suddenly leap up again, as we’ve become accustomed to seeing of late,” Berglund said.

Splash reported late last month on how spot rates on the transpacific had fallen below long-term contracted rates leading many shippers to start to look at the fine print of their contracts.

Xeneta disclosed today that it ran a survey of its customer base in July and found that many were now looking to renegotiate contracted rates given the recent spot market drops.

Berglund commented: “Our customers, mainly large volume shippers, now find themselves in a stronger negotiating position.”

The survey showed that 44% no longer feel confident in the stability of long-term contracts – of that 44%, some 22% said they were more likely to allocate lower volumes only to cheaper contracts, while 22% preferred to move allocation to the spot market as soon as prices dip below long-term rates.

Many analysts have been discussing the peak of the container bull-run this month.

“[T]he post-Covid demand boom appears to have run its course,” Drewry stated in a recent report with many nations around the world battling high inflation and some of the world’s largest shippers indicating lately inventory overstocking.

Drewry is still predicting carriers will make improved profits over the records set in 2021, and that supply chain constraints will persist through the first half of next year.

“While we should stress that we believe it is too early to confidently declare that there will be no 2022 peak season, the continued signs of market weakness … are hard to miss: Spot rates tumbling faster than seasonality, congested capacity being re-activated, contracts being reopened, rate declines not driven by capacity injection, and … continued sluggish demand, utilisation dropping below the ‘magic’ rate-rocketing level, and a return to normal in US consumer demand for durable goods,” Sea-Intelligence stated in a mid-July report.

“The signs are all suggesting a return to a more balanced market,” Sea-Intelligence reckoned, going on to predict the potential return of blank sailings if volumes dry up.

Looking at the average vessel utilisation on the head haul of each of the major east-west trades shows nominal utilisation dropping below the levels which previously sustained the higher rates during the pandemic.

On the transpacific utilisation rates have dropped below the 90% level for the first time since mid-2020, according to Sea-Intelligence who said that this implies that capacity is finally beginning to open up. On Asia-Europe, meanwhile, utilisation rates are back below 80%.

Sea-Intelligence pointed out on Sunday that boxship trading distances are turning negative.

“When trading distances increase, this also increases the need for vessel capacity and vice-versa. During the post-pandemic period, this led to an added need for capacity, however in recent months this effect has turned negative,” Sea-Intelligence pointed out, adding: “As the current market is clearly on a downwards trajectory in terms of supply/demand balance, this shift in sailing distance impact once more becomes an added element, pushing the development – this time downwards.”

Highly elevated spot rates on major ocean trade lanes have passed their peak, but shippers should expect short-term prices to settle at two to three times pre-pandemic levels for the foreseeable future, the CEO of logistics giant Kuehne+Nagel said while unveiling record interims on Monday.

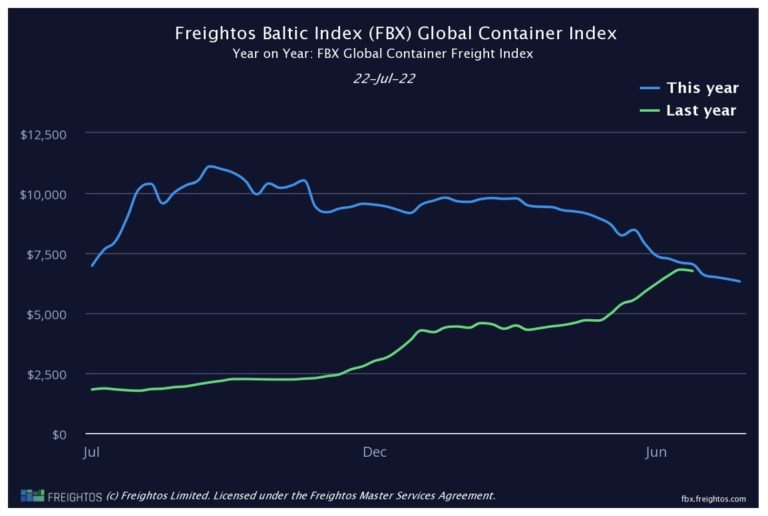

“Despite the falling prices, there are signs that ocean carriers don’t view this trend as the start of a complete collapse. Continued elevated rates for secondhand and chartered container ships show ocean carriers are still looking for capacity. Carriers have also scheduled 20% more transpacific capacity through October compared to last year,” commented Judah Levine, head of research at Xeneta rival, Freightos.

Sam Chambers